We explain why property prices rise, focusing on the key drivers such as low supply and high demand. Understanding these factors is vital for making informed investment decisions. Once you grasp what influences property values, you’ll be able to invest intelligently and use this knowledge to your advantage.

What You Will Learn

- The three key drivers of property prices.

- How credit availability and interest rates affect the market.

- The role of market sentiment in price changes.

- The impact of other factors on property price growth.

- How to make informed investment decisions based on long-term trends.

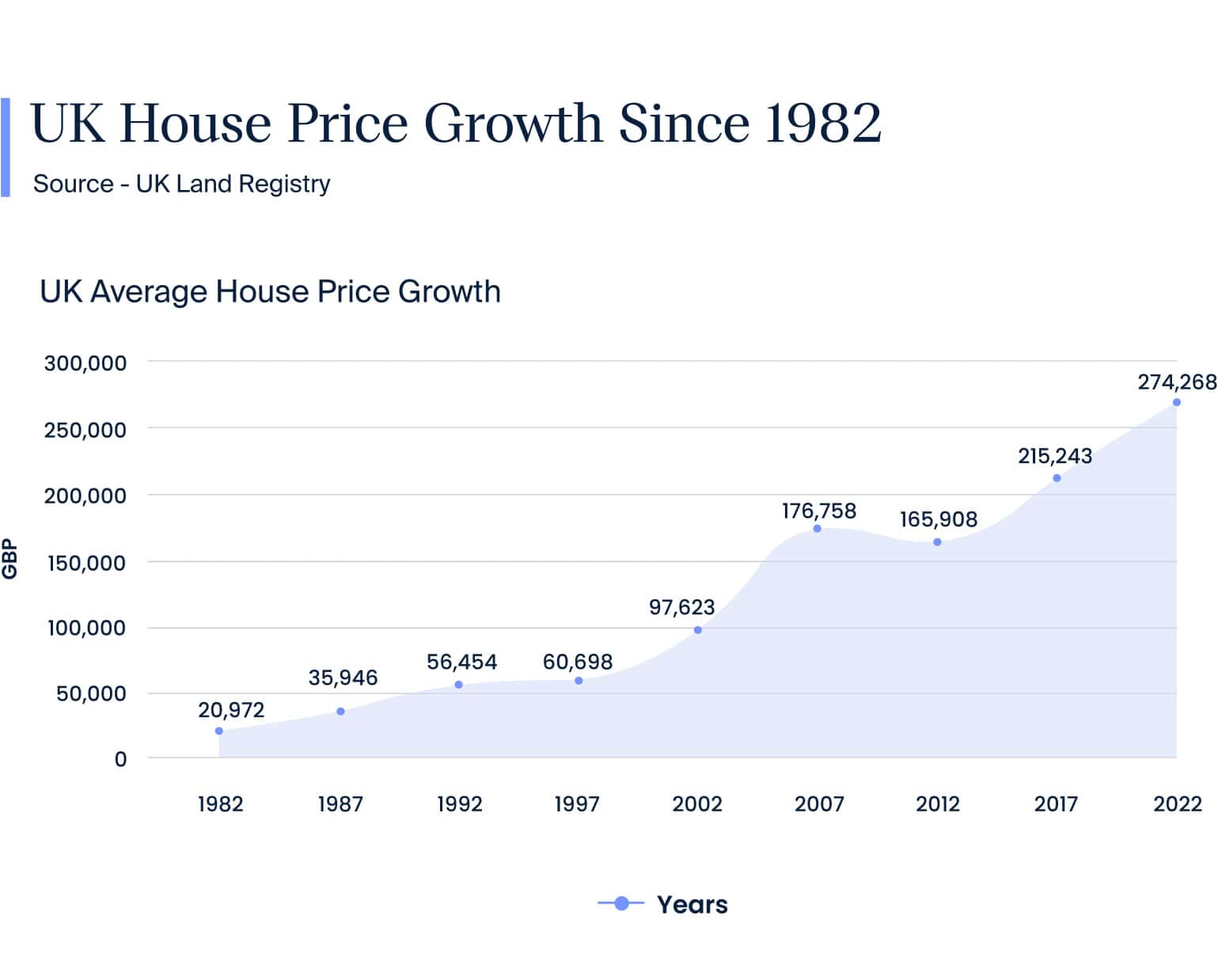

According to the UK Land Registry, UK house prices have increased consistently over the last 40 years. However, looking at the image below, it is essential to understand that the growth over the previous 40 years hasn’t been linear.

There are periods of both aggressive growth and where growth has levelled off and even fallen.

Understanding the core economic principles as to why we see growth in house prices, whether in the UK or elsewhere in the world, is extremely important when deciding to invest in a particular housing market.

Proven Property Investing Strategy for Expats

At Titan Wealth International, we offer a complete end-to-end property investment service for expats, guiding clients through every step, from legal and lending to letting, limited company incorporation, tax advice, and HMRC reporting.

What Causes Property Prices to Rise?

Multiple factors can affect property prices; however, there are three fundamental principles:

- Supply and demand.

- Credit availability.

- Sentiment.

Supply and Demand

Supply and demand is a crucial factor in causing property prices to rise. This is probably the most well-known fundamental that drives the price growth of an asset.

In addition, supply and demand will dictate when prices move over the long term:

- High demand: Competition for houses is fierce, driving prices higher.

- Low demand: When in an economic downturn and credit is more difficult to get, house prices can drop because the demand to buy a house is lower.

UK Housing Shortage

In the UK, it is widely known that there are not enough houses built to keep up with the demand.

For example, the Barker report released by the government in 2005 stated that in the UK, they needed to build 240,000 additional dwellings to facilitate the demand.

From 2005 to 2015, the number of houses built continuously missed the target. By the end of 2015, the number was revised to 300,000 new homes per year.

The latest release from the UK National Housing Federation stated that the UK now needs to build 340,000 homes annually until 2031.

In terms of demand, several key drivers have meant demand has consistently outpaced supply in the UK:

- Population growth: The UK population is projected to grow to 70,000,000 by 2030.

- Social factors: Divorce rates have increased, and the average household size has decreased by 23% since 1975.

- Property investment: 4.5 million UK households rent privately. This number has almost doubled from 2.5 million in 2006.

The chronic undersupply and ever-increasing demand in the UK housing market will continue to cause upward pressure on prices over the long term.

Exploring What Drives Property Prices Up?

Calculator

Property Investment Calculator

Maximise your property investment strategy with our comprehensive property investment calculator. Make informed decisions whether setting your purchase price or calculating investment requirements.

Credit Availability

The availability of credit via mortgage finance is a crucial factor in determining house prices. Mortgages have a significant impact on the housing market. Most buyers will use mortgage finance, whether you are an investor or someone buying a residential home.

When mortgage finance is readily available to homebuyers and investors at competitive interest rates, it encourages them to buy, increasing the demand and, in turn, rising house prices.

Example:

Grant is looking to purchase his first home, and the property’s value is £100,000.

In property market A, Grant can achieve an 80% loan to value mortgage, meaning his equity is £20,000.

In property market B, less credit is available, and the maximum loan to value Grant can achieve is 20%. He would need to put £80,000 down as a deposit to purchase the same property.

It is, therefore, more accessible and more affordable for Grant to purchase property in property market A.

Interest Rates

Interest rates will also impact the housing market. Again, let’s use the two-property market examples as above.

In property market A, you could borrow money at 2%. In contrast, in property market B, interest rates are higher, and the cost of borrowing is 8%.

Taking out mortgage finance in property market A is a much more viable option. It would be more appealing for Grant to buy a house.

What Happens to House Prices When Credit Availability is Low?

If credit and mortgages become less available and more expensive, and inflation is high, it directly impacts housing prices – find out how inflation can be a property investor’s best friend.

A great example is how the 2008 global financial crisis – also known as the credit crunch – impacted property prices.

Property prices fell in value during this period mainly because banks were more cautious, lending criteria were tightened, and lending became expensive.

This combination resulted in people struggling to get a mortgage, meaning less demand in the market and consequently, prices fell between 2007 and 2012.

The above highlights why understanding supply and demand is so important, as they significantly impact house prices. You should understand mortgage availability in the market you are investing in, even if you are not using mortgage finance to buy a property.

Book Your Complimentary Property Investment Call

During your 15-minute consultation, you will:

- Receive personalised advice to develop an expat investment strategy.

- Navigate the UK property market with our expert end-to-end service.

- Learn how to build a hands-off, long-term property portfolio for lasting success.

Sentiment in the Property Market

How people feel about their circumstances, the current state of the economy and the housing market is a key reason property prices rise.

It is human nature to think short term rather than long term, which is why sentiment and how people feel at any given time are so important.

Whatever the long-term factors are, excessive positivity or negativity will influence what people do now.

If people are pessimistic about the housing market and believe prices will fall. In that case, they will be less likely to buy a house and price growth will stagnate and potentially even fall.

Likewise, when sentiment is positive, buyers are more likely to take action, resulting in house prices rising because of increased activity.

The media heavily dictate sentiment. Despite a housing market having solid fundamentals, the media can dictate how prices move in the short term by influencing sentiment.

As an investor with a medium to long-term view, it is essential to focus on the fundamentals driving the market and not be swayed too heavily by headlines in the media.

What Other Factors Can Drive House Price Rises?

Several other factors can determine house price rises:

- The 18-year property cycle.

- Rent and wages.

- New infrastructure.

- New business.

Understanding the 18-year property cycle and what stage we are within the cycle can help you make a more informed property investment decision.

The relationship between rent and wages is also worth understanding. When wages rise, rents follow, which means more buy-to-let investors are willing to pay more for properties.

In areas with a local wage increase, investment in infrastructure and new businesses relocating to the area will see property prices rise.

Key Takeaway

We’ve explored supply and demand, credit availability, and sentiment as the key drivers behind why property prices rise. It’s important to recognise that these factors work together, not in isolation.

While no one can predict short-term market fluctuations with certainty, understanding these key drivers will empower you to make confident, informed investment decisions.

Even if property values dip, long-term trends should lead to recovery and growth once you grasp the fundamentals of why property prices rise.

Book a complimentary consultation to receive expert guidance on making smart property investment decisions based on these key principles.

The information provided in this article is not a substitute for personalised financial, tax or legal advice. You should obtain financial advice and tax advice tailored to your particular circumstances and in respect of any jurisdictions where you may have tax or other liabilities. Titan Wealth International accepts no liability for any direct or indirect loss arising from the use of, or reliance on, this information, nor for any errors or omissions in the content.