Book a Discovery Call

Find out how we can help you in 15 minutes.

Clients We Help Overview

British Expats

Wealth management for British expats, covering UK pensions, tax optimisation, and cross-border advice.

US Expats

Wealth management for US expats, including 401k rollovers, IRA transfers, and cross-border tax planning.

Non-Resident Indians

Wealth management for NRIs, addressing foreign tax obligations, remittances and currency fluctuations.

Financial Planning Overview

Create a personalised financial plan that brings together your pensions, investments, tax, and retirement goals into one clear strategy.

Education Fee Planning

Plan ahead for education costs with tailored strategies that help fund school and university fees while protecting your long-term wealth.

Major Life Event Planning

Navigate major life events with expert financial planning, helping you adapt your strategy as your personal and financial circumstances change.

Retirement Planning Overview

Build a retirement plan that helps you grow your wealth, generate sustainable income, and achieve financial confidence wherever you retire.

Retirement Income Planning

Create a sustainable retirement income strategy that helps you meet your lifestyle goals while managing tax, longevity, and investment risks.

Retirement Accumulation Planning

Grow your retirement savings with a tailored accumulation strategy designed to maximise long-term wealth and prepare you for retirement.

Pension Advice Overview

Make informed pension decisions with expert advice on retirement planning, consolidation, transfers, and managing pensions across borders.

Defined Benefit Pension Analysis

Understand your defined benefit pension with a detailed analysis of transfer options, retirement income, and long-term financial outcomes.

National Insurance Contributions (NICs)

Protect your UK State Pension by understanding your National Insurance contribution options while living and working overseas.

SIPP Advice

Maximise your retirement savings with tailored SIPP advice, helping you choose investments and manage your pension with confidence.

QROPS Advice

Receive specialist advice on managing your existing QROPS, ensuring it remains aligned with your retirement goals and tax position.

Annuities

Secure a reliable retirement income with expert annuity advice tailored to your lifestyle, income needs, and long-term financial security.

Pension Transfer Overview

Transfer your pension with confidence through expert advice, helping you manage tax, investments, and retirement planning across borders.

Defined Contribution Pension Transfer

Understand your defined contribution pension transfer options and make informed decisions to support your long-term retirement goals.

SIPP Transfer

Transfer your pension into a SIPP for greater investment flexibility, control, and retirement planning opportunities.

401k Rollover

Roll over your 401(k) with specialist cross-border advice, helping you manage tax, investments, and retirement objectives.

UK Pension Transfer Advice By Country

Explore your options for transferring a UK pension overseas, with country-specific guidance and specialist cross-border advice.

US Retirement Account Advice by Country

Access country-specific guidance on managing US retirement accounts while living overseas, including tax and retirement planning considerations.

Tax Planning Overview

Receive tailored cross-border tax planning advice to help you understand your tax position and make informed financial decisions.

General Tax Planning

Explore cross-border tax planning considerations with personalised advice tailored to your circumstances and financial objectives.

UK Repatriation Tax

Prepare for your return to the UK with tailored tax planning advice to help you understand the financial implications of repatriation.

Inheritance Tax

Understand the inheritance tax planning options available to you and receive tailored advice based on your circumstances and objectives.

Estate Planning Overview

Plan for the future with tailored estate planning advice to help you structure your affairs and communicate your wishes clearly.

Will Writing

Prepare a legally valid will with specialist guidance tailored to your personal circumstances, family needs, and international assets.

Trust Planning

Explore trust planning options with specialist advice tailored to your financial objectives, family circumstances, and estate planning needs.

Protection Planning Overview

Explore protection planning solutions designed to help provide financial security for you and your family if the unexpected happens.

Critical Illness Insurance

Understand your critical illness cover options with tailored advice to help support your financial needs following a serious illness.

Income Protection

Explore income protection solutions designed to provide financial support if illness or injury prevents you from working.

Asset Structuring Overview

Explore asset structuring solutions designed to support your cross-border financial planning, investment strategy, and long-term wealth objectives.

Personal Portfolio Bonds

Understand how Personal Portfolio Bonds can support your investment strategy and broader cross-border financial planning objectives.

Migration & Relocation Advisory Services Overview

Plan your international move with tailored guidance across relocation, residency, investment, and cross-border financial planning considerations.

Global Mobility Planning

Receive guidance on the financial and practical considerations of moving overseas, tailored to your circumstances and long-term objectives.

Citizenship by Investment

Explore citizenship by investment options with guidance on eligibility, application considerations, and how they may fit your wider plans.

Golden Visas (Residency by Investment)

Understand golden visa options with tailored guidance on residency routes, investment requirements, and wider financial planning considerations.

Expat Financial Advice: How to Manage Your Finances Abroad

Investment Management Overview

Grow and protect your wealth with tailored investment management solutions, designed around your financial goals, risk profile, and long-term objectives.

Portfolio Management

Access professionally managed portfolios tailored to your goals, risk tolerance, and time horizon, with ongoing monitoring and expert investment oversight.

Managed Portfolio

Invest in professionally managed, risk-rated portfolios with ongoing monitoring and rebalancing to keep your investments aligned with your objectives.

Custom Investment Portfolio

Create a bespoke investment portfolio tailored to your financial goals, risk preferences, and personal investment requirements.

Investment Accounts

Choose from a range of investment accounts designed to help you invest tax-efficiently while supporting your long-term financial goals.

Banking Solutions

Access international banking solutions tailored to expats, helping you manage your money seamlessly across borders with confidence.

Private Banking

Access bespoke private banking services, combining personalised wealth solutions, exclusive banking facilities, and dedicated relationship management.

Expat Banking

Manage your finances internationally with banking solutions designed for expats, offering flexible accounts and seamless cross-border banking.

Currency Transfer

Transfer money internationally with competitive exchange rates, efficient payments, and expert support for cross-border transactions.

Lending

Access tailored lending solutions to support property purchases, refinancing, and other borrowing needs wherever you live.

Property Investment

Access end-to-end property investment solutions, combining sourcing, financing, and structuring to help build long-term wealth through property.

Property Investment

Limited Company Incorporation

Set up a limited company for property investment, helping optimise ownership structures, tax efficiency, and long-term wealth planning.

Property Investment Developments

Explore carefully selected property developments for expats offering strong investment potential, with expert support throughout the process.

Investment Management for HNW Families: How to Build a Robust Family Wealth Programme

Expat Solutions Overview

Optimise My Tax Strategy

Tax optimisation solutions for expats, reducing liabilities with specialist cross-border advice.

Optimise My Portfolio

Optimise your portfolio with expert management, global access, and a strategy aligned to your goals.

Consolidate My Pensions

Consolidate your pensions for streamlined management and better investment options.

QROPS Pension Transfer to SIPP

Review your QROPS and discover if moving to a UK SIPP offers greater flexibility and value.

See All Resources

Articles

Read expert adviser-written articles on wealth management, tax, pensions, and expat financial strategies.

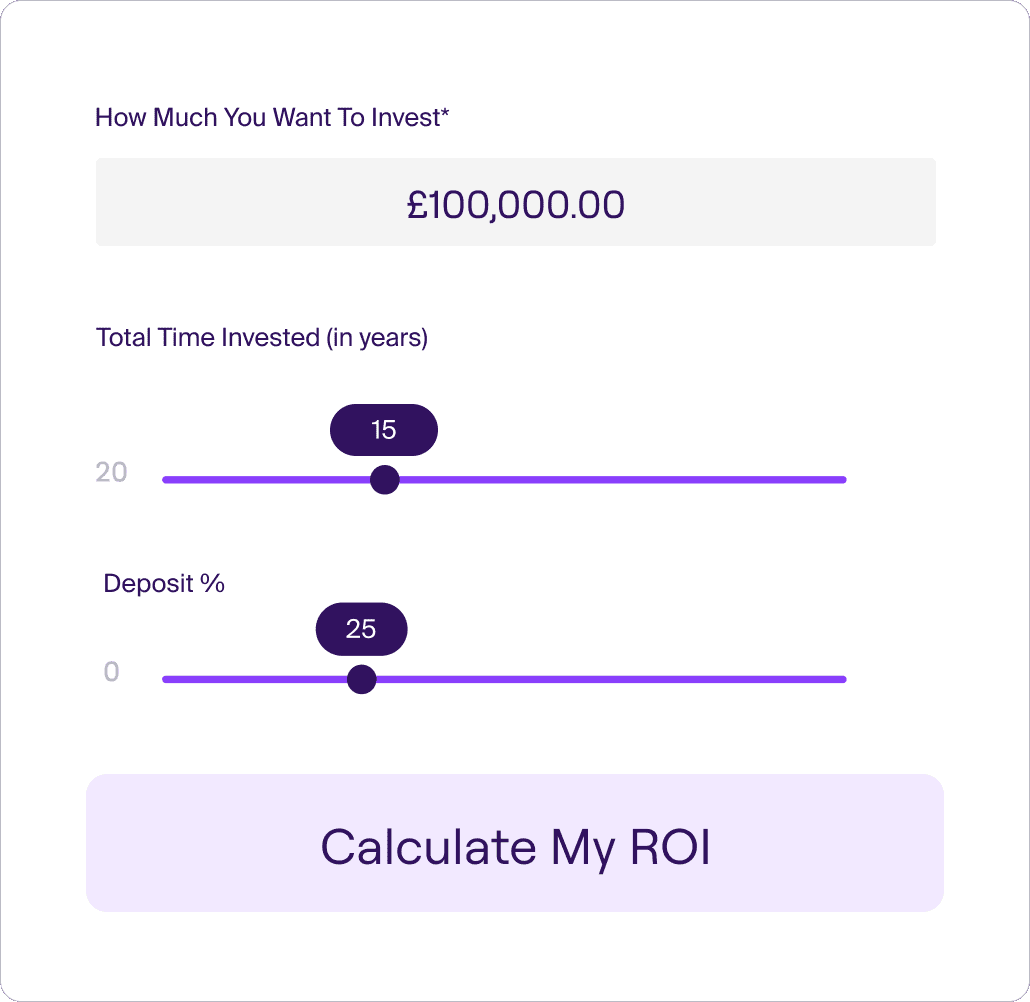

Calculators

Our calculators help you plan retirement, tax, pensions, and property investments to make informed financial decisions.

Guides

Discover expert guides on expat pensions, tax, property, and retirement planning to help secure your financial future.

Thought Leadership

Expert insights from our advisers and board on UK tax changes, expat wealth planning, global investing, and cross-border strategy.

Get clarity on how your final salary pension fits into a flexible, holistic retirement plan, whether you remain in the scheme or consider whether a transfer may be appropriate. We’ll model both scenarios, helping you weigh the income certainty of your defined benefit pension against the potential flexibility, risks and trade-offs of transferring. Our analysis factors in your life as an expat today and your future goals, including retiring abroad.

As Seen In

With a defined benefit pension, spouse or dependant benefits are usually set by the scheme rules and may be lower than the member’s pension. A personal pension can give you more flexibility over who may receive any remaining fund after your death, subject to pension rules, tax treatment, investment performance and the value left in the pension.

Defined benefit pensions are backed by the scheme and the sponsoring employer, and eligible UK schemes may also have Pension Protection Fund protection if the employer becomes insolvent. Funding levels, employer strength and PPF protection should be reviewed on a scheme-specific basis before deciding whether a transfer is appropriate.

A defined benefit pension provides a guaranteed income, usually for life and often with inflation-linked increases. Transferring to a personal pension may allow more flexible withdrawals, but you give up the guaranteed income and take on investment, inflation, longevity and withdrawal risk.

Unlike the fixed structure of a defined benefit scheme, a personal pension may give you more control over how your pension is invested, how income is taken, and how retirement withdrawals are planned. This flexibility can be valuable for expats, but it also means your retirement income will depend on market performance, charges, tax rules and how long the fund lasts.

Where appropriate, consolidating pensions from previous employment can make your retirement assets easier to manage and review. Some personal pensions may also offer access to wider investment options and multiple currencies, which can help expats manage currency exposure. Consolidation is not suitable in every case and may mean giving up valuable guarantees or scheme-specific benefits.

Defined benefit pensions usually pay a regular taxable income according to the scheme rules. A personal pension may allow more control over when and how withdrawals are taken, which can support tax planning. However, the tax treatment will depend on UK rules, your country of residence, any applicable double tax treaty, and your personal circumstances.

Defined benefit pensions often have a normal retirement age, commonly 60 or 65, and taking benefits early may reduce the income payable. Personal pensions can currently usually be accessed from age 55, but this rises to 57 from 6 April 2028 unless a protected pension age or another exception applies. Accessing pension funds earlier can reduce long-term retirement income.

A defined benefit scheme may offer a tax-free lump sum, depending on the scheme rules and commutation terms. If you transfer to a personal pension, you may be able to access part of the fund as a UK pension commencement lump sum, subject to UK allowances, scheme rules and any protections. For expats, this may still be taxable in your country of residence, so local tax advice is essential.

We specialise in financial advice for British expats, with services designed around the practical realities of living, working and retiring overseas. Our advisers are experienced in cross-border financial planning, including UK pensions, tax considerations and estate planning, helping you understand your options clearly and avoid unnecessary tax or planning mistakes.

Each client is supported by an experienced adviser who understands the complexities of defined benefit pension analysis for expats. Where regulated pension transfer advice is required, this must be provided or checked by an appropriately authorised pension transfer specialist. We help coordinate the process, explain the paperwork, and bring together Titan Wealth International’s wider wealth, tax and estate planning resources where relevant.

Our advisers are fully licensed and regulated, committed to upholding the highest standards of compliance and trust. We work closely with regulators to ensure our services meet industry requirements and prioritise our clients’ best interests.

We clearly explain our fees, what they cover, and when they apply before you proceed. This helps you make informed decisions with confidence, including understanding the cost of any advice, transfer implementation, product, platform or ongoing service.

£30,000

£30,000

Transfer values above £30,000 usually require regulated pension transfer advice before safeguarded benefits can be moved into a flexible pension.

Personal pensions can currently usually be accessed from age 55, but this rises to 57 from 6 April 2028 unless an exception or protected pension age applies.

A QROPS transfer can face a 25% overseas transfer charge unless the right exemption applies. For expats, cross-border pension advice is essential.

Many DB schemes provide a spouse or dependant pension, often lower than the member’s pension and subject to scheme rules. A personal pension may offer more beneficiary flexibility, but the amount left will depend on withdrawals, investment performance, charges and tax rules.

From 6 April 2027, most unused pension funds and death benefits will fall within UK inheritance tax rules, making pension and estate planning more connected.

RPI reform from 2030 may affect some DB pensions with RPI-linked increases. The impact depends on your scheme rules, inflation measure, caps, floors and when your benefits were built up.

Cons

Limited flexibility: Income is usually paid according to the scheme rules, with limited ability to vary the amount or timing once benefits start.

Pros

Guaranteed income for life: A defined benefit pension provides a regular income, usually payable for life. This income is set by the scheme rules and is not directly dependent on investment market performance.

Cons

Currency exposure for expats: Defined benefit pensions are usually paid in sterling. If you live and spend in another currency, exchange rate movements can affect the value of your income.

Pros

Potential inflation protection: Many defined benefit pensions increase each year, although the index used, caps, floors and the benefits covered will depend on the scheme rules.

Cons

Early retirement reductions: Taking benefits before the scheme’s normal retirement age may reduce the income payable. This is usually an early retirement reduction rather than a penalty.

Pros

Trustee management: The scheme is managed by trustees and administrators, so you do not need to make investment decisions or manage withdrawals yourself.

Cons

Scheme-rule dependant death benefits: Death benefits are set by the scheme rules and may not match your wider estate planning wishes. A spouse or dependant pension may be lower than your own pension, and not all family members will necessarily qualify.

Pros

Longevity protection: Your income usually continues for life, even if you live longer than expected.

Cons

Inflation increases can vary: Inflation protection is not the same across all schemes. The index used, caps, floors and the period when benefits were built up can all affect future increases.

Pros

Potential dependant benefits: Many schemes provide benefits for a spouse, civil partner or eligible dependant after your death. The amount and eligibility depend on the scheme rules.

Cons

Less control over investment strategy: You do not choose how the scheme is invested. This removes personal investment responsibility, but it also means the scheme’s strategy cannot be tailored to your own preferences, currency needs or wider financial plan.

Pros

Potential Pension Protection Fund support: Eligible UK defined benefit schemes may have Pension Protection Fund protection if the employer becomes insolvent and the scheme cannot meet its liabilities. The level of protection depends on your circumstances and the type of benefits involved.

Pros

Clear retirement age: Most schemes have a normal retirement age, often 60 or 65. Early or late retirement may be possible, but the income may be adjusted under the scheme rules.

Cons

Loss of guaranteed DB income: Transferring usually means giving up a guaranteed income for life. This is a valuable benefit and a transfer is unlikely to be suitable for most people unless it can clearly be shown to be in your best interests.

Pros

Flexible withdrawals: A personal pension may allow you to vary how much income you take and when you take it, subject to pension rules, tax rules and scheme terms.

Cons

Investment and withdrawal risk: The value of a personal pension can rise or fall. Poor investment performance, market falls, high withdrawals or living longer than expected could reduce your future income or exhaust the fund.

Pros

More investment choice: You may have more control over how your pension is invested, allowing the strategy to be tailored to your objectives, risk profile and retirement plans.

Cons

Inflation risk: Unless you buy an inflation-linked annuity or manage withdrawals carefully, inflation may reduce the real value of your retirement income over time.

Pros

Potential currency flexibility: Some personal pensions designed for international clients may offer multi-currency options, which can help expats manage currency exposure.

Cons

Charges and advice costs: Personal pensions may involve product, platform, investment and advice charges. These costs can reduce the value of the fund over time.

Pros

Beneficiary flexibility: A personal pension may give you more flexibility over who can receive any remaining fund after your death, subject to pension rules, tax treatment and the value left in the pension.

Cons

Tax complexity for expats: Withdrawals may be taxed differently depending on UK rules, your country of residence and any applicable double tax treaty. From 6 April 2027, most unused pension funds and pension death benefits will also fall within UK inheritance tax rules.

Pros

Potential lump sum access: You may be able to take part of the fund as a UK pension commencement lump sum, subject to UK allowances, protections and scheme rules. For expats, this may still be taxable in your country of residence.

Cons

Usually irreversible: A transfer is usually irreversible. Once completed, the trustees are not normally obliged to reinstate your original defined benefit pension.

Pros

Blended retirement planning: A personal pension may allow you to combine flexible withdrawals with other retirement income sources, such as investments, rental income, state pensions or annuities.

Pros

Potential annuity option: You may be able to use some or all of the fund to buy an annuity and secure a guaranteed income. The income available will depend on annuity rates, age, health, options selected and whether inflation or dependant benefits are included.

Book a free, no-obligation 15-minute call to discuss your situation, where you live, your retirement goals and whether a defined benefit pension analysis may be relevant.

This call is designed to understand your needs and explain the next steps. It does not provide a transfer recommendation.

With your permission, we contact the trustees or administrators of your UK pension scheme and gather the information needed to understand your benefits.

This may include your scheme rules, Cash Equivalent Transfer Value, retirement options, spouse or dependant benefits, increases in payment, early retirement terms and any guarantees or restrictions.

Once we have your pension information, your adviser will discuss your financial situation, retirement goals and personal circumstances.

To do this, we will:

We provide a pension analysis report based on your scheme information and personal circumstances.

The report may include:

If regulated advice is required, any recommendation must be provided or checked by an appropriately authorised pension transfer specialist.

If a transfer is recommended and you choose to proceed, we will explain the implementation process, fees, receiving pension options and ongoing advice arrangements before any action is taken.

If a transfer is not recommended, we will explain why and help you understand the value and options available within your existing scheme.

Featured article

Transferring your final salary pension is an irreversible decision that requires careful consideration. This detailed guide explains everything UK expats need to know about the final salary pension transfer process, pension scheme alternatives, and potential downsides.

A pension transfer value (CETV) is the cash value that you would receive from your private sector defined benefit pension provider into your own personal pension. Find out your estimate in 30 seconds with our calculator.

A defined benefit pension is a valuable benefit, and deciding whether to remain in the scheme or explore a transfer requires careful analysis. During your 15-minute introductory call, we’ll discuss your circumstances as an expat, explain how the analysis process works, and help you understand the key factors that may affect your options.

During your call, you’ll:

Schedule your no-obligation call today to explore your options and plan confidently for your future.

A defined benefit pension, also known as a final salary pension, provides a retirement income based on the scheme rules. This is often linked to your salary, years of service and the scheme’s accrual rate.

Unlike a personal pension, the income is not based directly on your own investment pot. The scheme is responsible for paying the promised benefits, usually for life and often with inflation-linked increases.

Some British expats can transfer a private sector defined benefit pension, subject to scheme rules, statutory conditions and regulated advice requirements.

If your safeguarded benefits are valued above £30,000, you will usually need appropriate independent advice before transferring to a flexible pension arrangement. Some schemes, including many unfunded public sector schemes, generally cannot be transferred to flexible arrangements.

Not for most people. A defined benefit pension is a valuable benefit because it usually provides a guaranteed income for life.

A transfer may be suitable in some circumstances, particularly where flexibility, currency planning, beneficiary planning or international tax considerations are important. However, you would give up guaranteed income and take on investment, withdrawal, inflation, tax and longevity risk. A transfer should only proceed where regulated advice shows it is suitable for your circumstances.

A transfer to an overseas pension may be possible through a qualifying recognised overseas pension scheme, known as a QROPS. However, QROPS transfers are complex and may trigger a 25% overseas transfer charge unless an exemption applies.

The tax position will depend on your country of residence, the country where the QROPS is established, the timing of the transfer, the receiving scheme and any future change in your circumstances.

Yes, in some cases. A SIPP is a UK pension, so it does not move your pension to another country, but it may allow you to manage your pension while living overseas.

Whether a SIPP, QROPS or remaining in your DB scheme is more appropriate will depend on your country of residence, tax position, retirement plans, currency needs, transfer value, scheme benefits and risk profile.

Yes. If you transfer out of a defined benefit pension, you give up the scheme’s guaranteed income, usually payable for life and often with inflation-linked increases.

A personal pension may give you more flexibility over investments and withdrawals, but it does not provide the same guaranteed income unless you use some or all of the fund to buy an annuity or another guaranteed-income product.

That depends on the type of pension and the scheme rules.

Defined benefit schemes usually provide benefits for a spouse, civil partner or eligible dependant, but these benefits are normally set by the scheme and may be lower than your own pension. A personal pension can offer more flexibility over who may receive any remaining fund after your death.

However, this does not guarantee that a particular amount will be left. The value available will depend on withdrawals, investment performance, charges, tax treatment and the value remaining in the pension. From 6 April 2027, most unused pension funds and pension death benefits will fall within the value of a person’s estate for UK inheritance tax purposes.

Many defined benefit schemes have a normal retirement age, often 60 or 65. Some schemes allow earlier access, but the income may be reduced by an early retirement factor.

Personal pensions can currently usually be accessed from age 55, but this rises to 57 from 6 April 2028 unless a protected pension age or another exception applies. Taking pension benefits early can reduce the income available later in retirement.

We understand that losing guaranteed benefits, such as a lifetime income, can be a concern when considering a transfer from a defined benefit pension.

The Cash Equivalent Transfer Value, or CETV, is the cash value offered by your scheme in exchange for giving up your defined benefit pension. It can be used to explore whether a personal pension, annuity, or blend of both could meet your retirement income needs.

It may be possible to transfer your benefits and use some or all of the pension fund to buy a guaranteed income in the form of an annuity. In some cases, an annuity may provide a higher starting income than your defined benefit pension, particularly where single-life terms, health, lifestyle factors or reduced death benefits are relevant.

However, the income available will depend on annuity rates, your age, health, options selected, inflation-linking, spouse or dependant benefits, and the currency in which income is paid.

If you want guaranteed income but do not need all of the income offered by your defined benefit scheme, using part of a transferred pension to buy an annuity and leaving the rest invested could provide a blend of guaranteed income and flexibility.

Please note that your scheme’s guaranteed income is a valuable benefit. You should only consider giving it up if a regulated analysis shows it is suitable for your circumstances and you have sufficient secure income to meet your essential retirement expenditure.

Yes. Tax can be one of the most important factors for British expats considering a defined benefit pension transfer.

The position may depend on UK pension rules, your country of residence, any applicable double tax treaty, the receiving pension type, how and when you access benefits, and future changes in tax law. A QROPS transfer may also trigger the 25% overseas transfer charge unless an exemption applies.

You should take cross-border tax advice before transferring or accessing pension benefits.